The Family Mortgage

Helping buyers with a low deposit to purchase a property, using security provided by their family.

View product details

Buying a home with help from family members

The principle behind our family assisted mortgage is simple. It helps families help their family members take the first step on the property ladder.

- You own the property

- You only need at least a 5% deposit, with family members willing to bring your total deposit up to 25% using additional security in the form of their savings, property value or a mixture of the two.

- You may be able to get a lower interest rate that might otherwise be available for a 95% LTV mortgage, meaning lower monthly payments.

How it works

Watch our short video that explains how the Family Mortgage works:

How it works for home buyers

You own the property

No matter who has helped, you have the legal rights to the property.

You will need at least 5% deposit (which can be wholly gifted) and family members who are willing to provide additional security, for up to 10 years, bringing the total deposit up to 25%.

A more affordable mortgage

Any additional security held in our Family Offset Account reduces the amount of the mortgage on which interest is charged.

After 10 years the Family Mortgage is reviewed. As long as the mortgage has been kept up to date, family members will have their money returned.

Fixed monthly payments

We offer 5 year fixed family mortgage rates, giving you the security and certainty of what you need to pay.

Calculate the security needed and your monthly repaymentsUnemployment Cover included

Subject to meeting certain conditions, and if you became unemployed through no fault of your own, we’ll meet your mortgage payments for up to six months on a one-off basis while you get back on your feet.

How it works for family members

Family friendly mortgage

Family members can use their savings or equity in their home for up to 10 years as additional security for the mortgage. It doesn't have to be parents, it could be a grandparent or step-relation.

Additional security assets must bring the total deposit up to 25%.

Provide additional security in three ways

Put your savings in our Family Security Account which earns interest.

Put your savings in our Family Offset Account reducing the amount of the mortgage on which interest is charged.

Any combination of these security options can be used.

Commitment for 10 years

You will need to be willing to put aside your savings or equity in your home as security for up to 10 years.

By offering security for the mortgage you are responsible for making up any shortfall if the property is sold for less than the mortgage value.

How to apply

Contact our friendly New Business Team:

Call us on 03330 140144 Ask us to call back Email us Complete our enquiry form

Family Mortgage repayment calculator

Calculate the security you and your family will need and what your monthly repayments could be.

Calculate the security needed and your monthly repayments

The security options available with the Family Mortgage

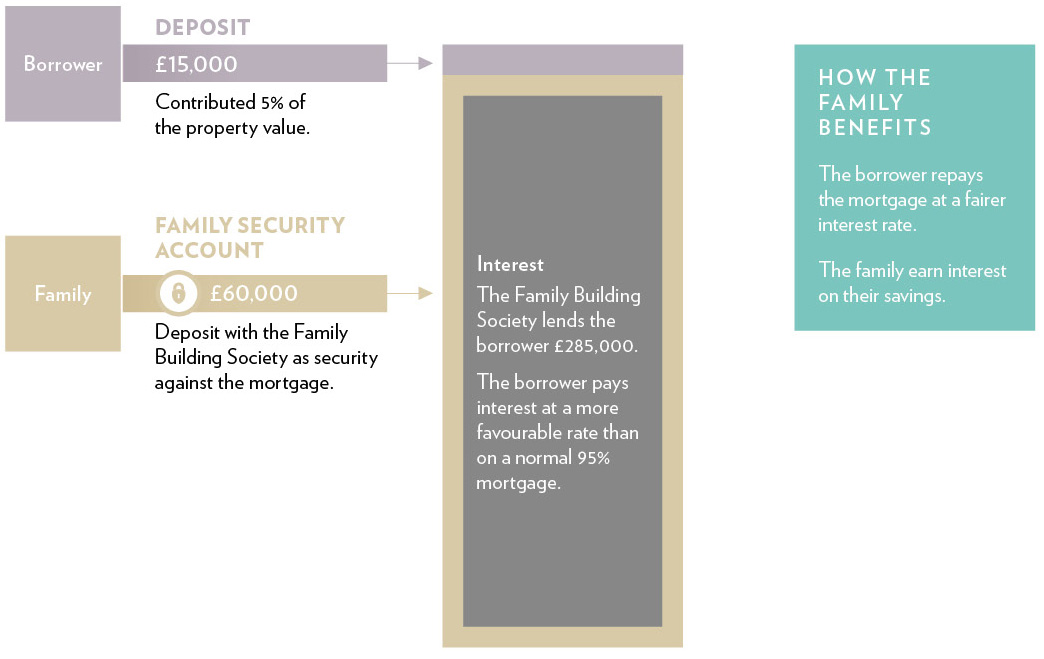

Family Security Account

Family members can provide security for the borrowers mortgage by depositing their savings in our Family Security Account.

How it works:

- The money acts as security for the mortgage.

- We can offer a mortgage at a more favourable interest rate.

How the family benefits:

- Savings in our Family Security Account earns the family interest.

The arrangement will be reviewed at the end of each fixed rate period up to 10 years. At the end of the 10 years, as long as the mortgage is up to date, the family members will have their money returned.

An example

Value: £300,000. A buyer has £15,000 for a 5% deposit. He needs to borrow £285,000. To bring the total deposit up to 25% his family have savings of £60,000 that they want to use to help their son buy his first home.

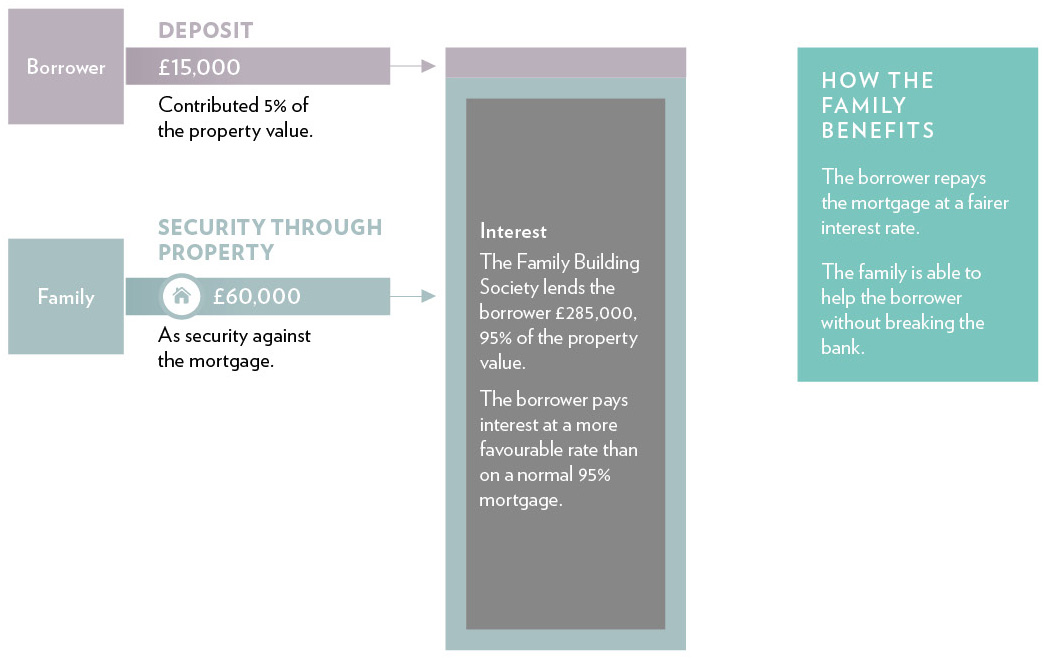

Security through Property

Family members can provide a charge over some of the value in their property, so there's no need for them to use their savings.

How it works:

- The money acts as security for the mortgage.

- We can offer a mortgage at a more favourable interest rate.

How the family benefits:

- If the family doesn't have any savings this may be a more suitable alternative.

The arrangement will be reviewed at the end of each fixed rate period up to 10 years. At the end of the 10 years, assuming the mortgage is up to date, the charge on the family's property comes to an end.

An example

Value: £300,000. A buyer has saved £15,000, a 5% deposit. She needs to borrow £285,000. She needs a further £60,000 so she has a total deposit of 25%. Her family doesn't have any savings to spare but are happy to use some of the value of their home (£60,000) as security.

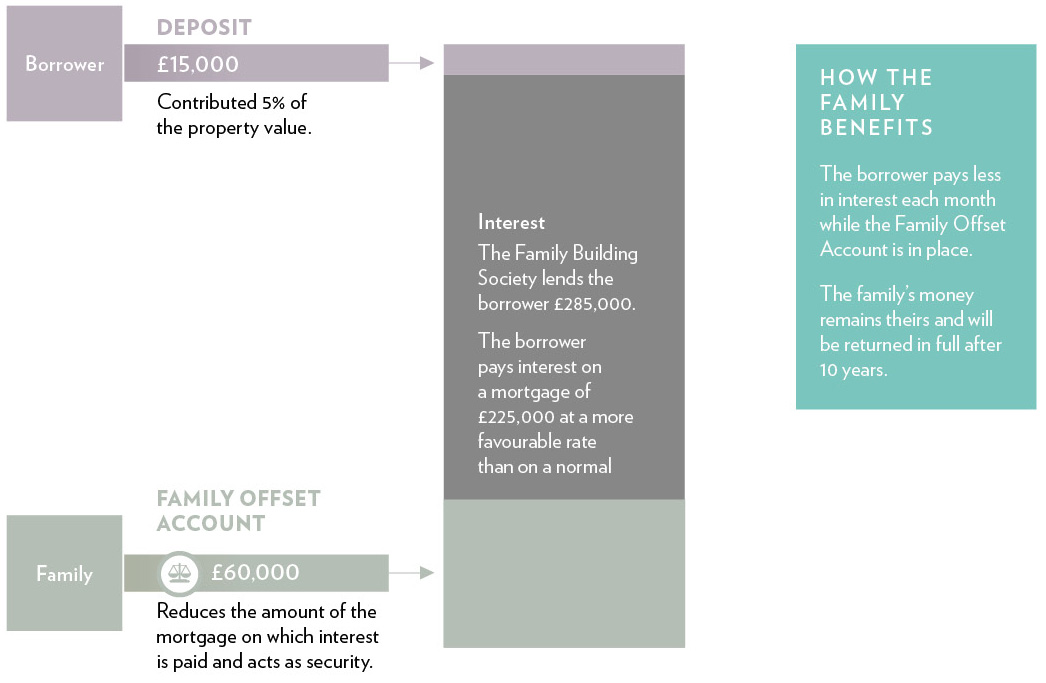

Family Offset Account

Family members can place their savings into a Family Offset Account which is linked to the Family Mortgage. This helps to reduce the amount of the mortgage on which interest is charged.

How it works:

- The money acts as security for the mortgage.

- We can offer a mortgage at a more favorable interest rate.

How the family benefits:

- Reduced monthly mortgage payments for you.

- By not receiving interest on their savings (which may be subject to tax) the family are passing on a bigger benefit to you by saving interest on your mortgage.

The arrangement will be reviewed at the end of each fixed rate period up to 10 years. Assuming the mortgage is up to date then the family members can expect their money to be returned in full after 10 years.

An example

Value: £300,000. A buyer has saved £15,000, a 5% deposit. To bring the total deposit up to 25% the family place £60,000 in a Family Offset Account, reducing the amount of the mortgage from £285,000 to £225,000.

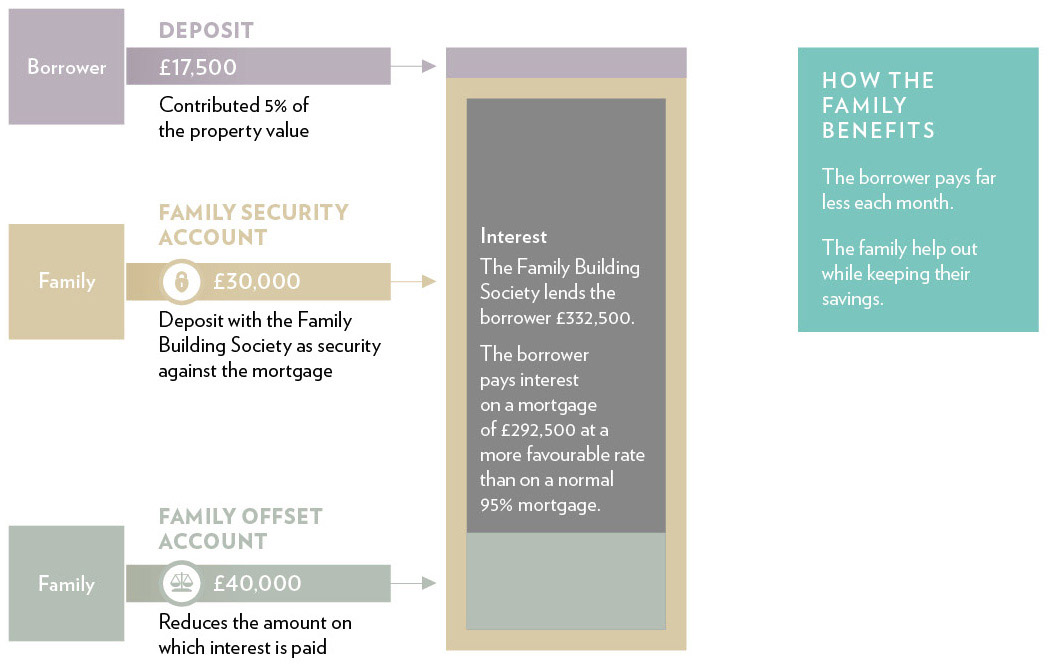

Using the security options in combination

Family members can pool their money together using any combination of the three additional security options to reduce mortgage costs.

How it works:

- The money acts as security for the mortgage.

- We can offer a fairer interest rate on your mortgage.

How the family benefits:

- Reduced monthly mortgage payments for you.

- The family can use either their savings or equity in their property as security to help you get the home you want.

The arrangement will be reviewed at the end of each fixed rate period up to 10 years. Assuming the mortgage is up to date then the family members can expect their money to be returned in full after 10 years.

An example

Value: £350,000. A couple have saved £17,500, a 5% deposit. They require a further £70,000 to bring the total deposit up to 25%. One of the parents deposit £30,000 in our Family Security Account as security against the mortgage. The other parents put £40,000 into our Family Offset Account. This reduces the amount on which interest is charged by £40,000, from £332,500 to £292,500.

Find out more

Get in touch

Contact our friendly New Business Team:

Call us on 03330 140144 Ask us to call back Email us Complete our enquiry form

Family Mortgage repayment calculator

Calculate the security you and your family will need and your monthly repayments.

Bank of Mum and Dad

Helping loved ones onto the property ladder? We have created a series of simple guides on how to run the Bank of Mum and Dad and important things you need to consider.

Representative example

A mortgage of £304,688.00 payable over 33 years initially on a fixed rate for 5 years at 5.04% and then on our variable Managed Mortgage Rate, currently 7.69% would require 63 monthly payments of £1,580.24 and 333 monthly payments of £2,055.43 plus one initial interest payment of £1,309.81.

The total amount payable would be £786,197.12 made up of the loan amount plus interest of £480,635.12, an Application Fee of £175, a Product Fee of £599 and a Mortgage Exit Fee of £100.

What is a representative example?

This is an illustration of a typical mortgage and its total cost.